Medicare Plan G is one of the most popular choices for consumers as they look to purchase a Medicare supplement. While Plan N often makes a lot of sense on paper when you look at past rate increases and the lower premium in general, so why are more people truly buying Plan G over Plan N? And how do we know that’s actually what they’re buying these days?

Telos Actuarial published an interesting study recently looking at the future of Medicare supplements. We broke down parts of the study and will talk about some of that here.

There are a few reasons why Plan G has become the more preferred option for many people as they choose their Medicare supplement.

As the cost of healthcare continues to rise and many individuals opt for Medicare supplement coverage, understanding the differences between these two plans is essential for choosing the best fit for your individual needs. In this article, we will explore why Medigap (aka Medicare supplement) Plan G is often the ultimate choice by consumers over Plan N when it comes to supplementing their original Medicare coverage.

First and foremost, Plan G offers broader coverage than Plan N does. After a consumer pays their Part B deductible, Plan G pays all further co-pays, co-insurance, and 100% of excess charges. How does Plan N differ? Plan N requires the consumer to pay that same Part B deductible, but Plan N does not cover excess charges and also requires the consumer to pay an “up to $20.00 co-pay for doctors office visits”. And, the final difference between Plan N and G is that Plan N will charge the consumer $50.00 should they go to an emergency room and not become admitted as an in-patient.

Let’s walk through what “excess charges” are. If a physician does not accept as full payment what Medicare will pay, they do have the opportunity to charge the consumer up to 15% more than the Medicare allowable amount. However, studies do suggest that approximately 95% of physicians do accept “assignment” (meaning they accept what Medicare pays as full payment thus no excess charge will result).

What we find is that with broader coverage of Plan G comes greater peace-of-mind knowing that you will be protected against unexpected bills due to medical emergencies, serious illnesses or other unforeseen expenses.

Let’s discuss the premiums related to these plan options. Plan N premiums will be lower than Plan G. How much lower? Well, if you are in Michigan? The pricing difference per month could be $25.00. If you are in Florida? The monthly difference between N and G could be $70.00. So, Plan N is often a more attractive choice in Florida over Michigan.

Another reason that Plan G is so popular these days is due to what is referred to as MACRA. The Medicare Access and CHIP Reauthorization Act of 2015. One of the results of MACRA was that under this new regulation, Medicare supplement policies are no longer able to provide coverage for the Part B deductible in policies sold to those newly eligible for Medicare as of January 1, 2020 or later.

Prior to January 1, 2020, a medicare supplement that is called Plan F was offered to consumers. Plan F pays the Part B deductible for the consumer and everything after that. Plan F required a person to pay a monthly premium and as long as Medicare approved a charge, Plan F would pay 100% of the remaining charge for the consumer. They pay/paid everything. Sounds pretty good, right?

Well, lots of people thought that also. They bought Plan F and loved it. After MACRA came along, those people new to Medicare as of 1/1/2020 were no longer able to buy the Plan F. So, what is the next best plan? Well, that is Plan G.

NOTE: The only difference between Plan F and Plan G is who pays the Part B deductible. Plan G policyholders pay the deductible whereas Plan F plan holders don’t have to pay the deductible. The insurance company does.

ALSO NOTE: Those that had purchased Plan F can remain in the Plan F and Plan F can still be purchased by those that were ELIGIBLE for Medicare prior to 1/1/2020.

But, after January 1, 2020, Plan G became the new leader in terms of Medicare supplement sales.

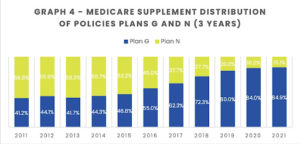

See the two graphs from the Telos Actuarial study below. The first chart shows that 71.3% of Medicare supplement sales in 2021 have become Plan G or Plan N.

And, further, this chart shows that 84.9% of people that buy Plan G and N purchase Plan G. 15.1% chose to purchase Plan N.

Plan G and Plan N – What People Are Buying

What do we see in our agency? The same. We have to agree with Telos.

Most people are certainly attracted to the lower premium with Plan N and with the historically lower rate increases over time. Who doesn’t want to keep premiums as low as possible over the long haul?

But, then comes the little thoughts in your mind “well, I’m getting older… what if I did get excess charges and they really added up?… What if I went to the doctors four times this month?” and more.

So, at the end of the day, many people just say “never mind, I’ll just go with a Plan G”.

Common question – Can I change to a Plan G if I start with a Plan N? Assume that you cannot. Most carriers in most states will require you to go through medical underwriting even if you stay with the same insurance company and just want to change letters so keep that in mind as you are choosing for the first time.

Our two cents? You can’t go wrong either way. Both Plan G and Plan N offer wonderful coverage to anyone enrolled into Medicare.

Joanne Giardini-Russell is a Medicare Nerd & the owner of Giardini Medicare, helping people throughout Metro Detroit and the country transition to Medicare successfully. Contact Joanne at joanne@gmedicareteam.com or by calling 248-871-7756.

Leave a Reply